For decades, accounting has been one of the most repetitive and time-consuming parts of running a business. Reconciling transactions, chasing missing receipts, and double-checking entries used to mean long hours, human error risks, and piles of coffee cups.

Today, AI in accounting is flipping that script. What once took days can now be done in minutes, with greater accuracy than ever before. Whether you’re a small business owner, a corporate finance leader, or an AI accountant in the making, artificial intelligence is changing not just how we do bookkeeping, but what we can do with the time it saves.

In this article, we’ll explore how AI is revolutionizing accounting and reconciliation, the benefits and challenges, real-world applications, and what it means for the future of accounting and artificial intelligence.

The accounting industry has always been quick to adopt technology from calculators to spreadsheets to cloud-based accounting software. But artificial intelligence in accounting is a leap forward. Instead of just processing numbers faster, AI can understand patterns, spot anomalies, and even make predictions.

Here’s why it’s such a game-changer:

Stat check: According to Accountancy Age, over 40% of accounting firms are now actively implementing AI tools for tasks like reconciliation and financial forecasting.

Artificial intelligence and accounting intersect in a variety of ways, from behind-the-scenes automation to client-facing services.

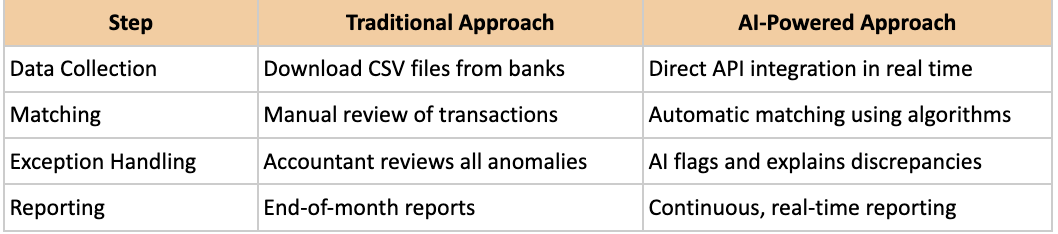

Reconciliation is one of the most time-consuming tasks in accounting. AI can compare bank statements to accounting ledgers and match transactions automatically flagging only the exceptions that require human review.

Example: An AI system spots that a payment for $1,235 appears in the bank statement but not in the accounting records. Instead of sifting through 500 entries, an accountant can review just the flagged discrepancy.

AI in accounting and finance can automatically classify expenses into categories like “Travel,” “Utilities,” or “Marketing” by analyzing descriptions, vendors, and transaction history. The more it learns, the more accurate it becomes.

Fraudulent transactions often hide in plain sight. AI excels at recognizing subtle anomalies like payments just under approval thresholds or unusual vendor patterns that could signal fraud.

By analyzing historical data, AI accounting systems can forecast cash flow, identify seasonal revenue trends, and even predict late payments from customers.

Reconciliation is often seen as a routine “box-ticking” process, but it’s actually critical for financial accuracy. Errors here can cascade into tax issues, compliance problems, and misinformed decisions.

One of the biggest concerns around artificial intelligence in accounting is whether it will replace accountants. The short answer: it won’t, but it will change their role.

Instead of spending hours on manual entry, accountants will:

Think of AI as the ultimate junior assistant, fast, precise, and tireless, while human accountants step into more consultative, higher-value roles.

Read More: AI in Accounting: Practical Applications, Trends & Tools

1. Speed and Efficiency

Tasks that took days can now take minutes, freeing up resources for strategic work.

2. Accuracy and Consistency

AI removes the risk of “fat-finger errors” and fatigue-related mistakes.

3. Cost Savings

By automating repetitive tasks, businesses can handle more work without increasing headcount.

4. Better Decision-Making

Real-time insights lead to faster, better-informed business decisions.

5. Scalability

No need to hire extra staff during busy seasons, AI can handle the workload.

While AI in accounting firms offers huge benefits, it’s not without its challenges:

A mid-sized e-commerce company processes thousands of transactions daily across multiple sales platforms. Using traditional reconciliation, their finance team spent over 30 hours each month matching transactions.

After implementing an AI Accounting Software:

The result? More time for financial analysis and better protection against errors and fraud.

The future of AI in the accounting industry is about moving from reactive to proactive.

As AI becomes more integrated, accountants will evolve into financial strategists, guiding clients through data-driven decisions.

The question isn’t “Will AI change accounting?” - it already has. The real question is “How will you use AI to your advantage?”

From bookkeeping automation to advanced reconciliation, artificial intelligence in accounting and finance is creating faster, smarter, and more reliable systems. The accountants of tomorrow won’t be buried in spreadsheets, they’ll be interpreting real-time insights, advising clients, and shaping financial strategies.